August 2025

What happened

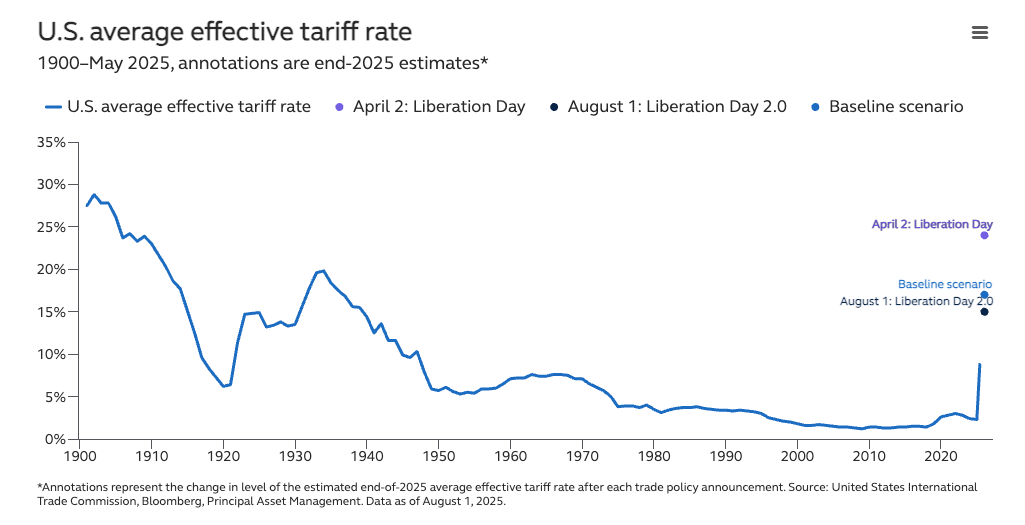

Today marks the delayed deadline for implementing reciprocal tariffs. Reciprocal tariffs, originally announced on April 2, also known as “Liberation Day,” saw U.S. import tariff rates rise significantly for over 50 trade partners before being temporarily lowered to 10% until July 9 to allow for negotiations.

Late Thursday night (July 31), President Trump signed an executive order announcing a new set of tariffs (thankfully alphabetized this time – small mercies). Reciprocal tariffs have been set at a 10% global minimum, with levies sitting at 15% or higher for countries that hold trade surpluses with the U.S. Several key trade partners, including the EU, Japan, and South Korea, have negotiated a 15% tariff. In contrast, others, such as China, Mexico, and Canada, face higher rates. Notably, the EU, Japan, and South Korea have carve-outs reducing the levy on autos from 25% to 15%. The tariffs are due to take effect after August 7.

Overall, the newly announced rates are lower than those announced on Liberation Day, but higher than the 10% baseline that had been in motion since late April when the 90-day reprieve was announced. The average effective tariff rate now sits at 15%, the highest level since the 1930s Smoot-Hawley tariffs and meaningfully higher than the 2% at the start of 2025.

Market reaction

The market response to the latest tariff announcements has been subdued relative to the post-Liberation Day reaction, and, overall, U.S. equities are sitting near their all-time highs, with global markets also much stronger than they were at the start of the year.

This likely reflects the fact that Trump’s tariffs have had a limited macro impact so far (although the latest jobs report does indicate greater weakness in the labor market), and the latest earnings season is showing earnings growth beating forecasts, suggesting that companies are navigating tariff headwinds without too much stress.

How does the tariff announcement compare with expectations?

|

So far, some country-level tariff announcements have been slightly more punitive than we and the broader market had anticipated, but less punitive on a sectoral basis. Our baseline expectations, as set out in the market bulletin “U.S. Tariffs: The end of the 90-day reprieve...”, was for the average effective U.S. tariff rate to ultimately settle at around 17%, slightly higher than the current level of 15%. There is potential for the effective tariff rate to rise further from here.

Even with the latest tariff announcements, trade-related headlines are unlikely to fade anytime soon. Since the newly announced tariffs won’t take effect until after August 7, there’s still time for additional trade deals to be reached in the coming week. Meanwhile, negotiations with China and Mexico remain unresolved, and the White House is expected to announce further sector-specific tariffs targeting industries such as pharmaceuticals and semiconductors. At the same time, ongoing legal challenges could weaken the durability of broad-based tariffs, potentially prompting the administration to focus more heavily on targeted, sectoral measures.

Also worth keeping in mind – the administration’s liberal use of tariffs as a negotiating tool to extract non-economic concessions means that tariff noise will likely remain a permanent feature of the economic backdrop for the remainder of this U.S. administration.

Macro impact

So far, the U.S. economy has held up relatively well, with activity data suggesting only a modest cooling in U.S. growth. However, July’s very weak jobs report suggests that the economy may already be feeling the brunt of tariffs. It’s worth remembering that, in a bid to beat the tariff shock, there was a significant front-loading of U.S. imports earlier in the year. Not only did this boost growth for many U.S. key trading partners, but it also cushioned the blow for both U.S. consumers and companies. However, that front-loading likely just postponed the economic fallout, rather than preventing it.

As stockpiles are run down and as new tariffs come into effect, someone will have to absorb the tariff: either the global exporters, the U.S. importers, or U.S. consumers. So far, data suggests that (for the imports that were subject to tariffs), few global exporters have absorbed the tariff increases.

U.S. growth: Our estimates suggest that the overall tariff impact would ultimately result in a 1.7% drag on annual U.S. GDP growth over the next few years. It is important, however, to note that there is significant variability around this estimate. While we assume that substitution effects—which see some tariffed goods trade flows replaced by domestic sources—could mitigate some of the adverse effects, other factors, such as behavioral or preference changes and currency movements, could also increase or reduce the growth impact of tariffs.

Inflation: Our baseline scenario also sees in a one-off tariff-induced boost to inflation of 1.6%, likely bringing core inflation up to 3.5% by year-end. While unlikely to lead to a persistent inflationary impulse, the Federal Reserve is rightly concerned that the impact could further fuel inflation expectations, especially as overall price stability remains elusive.

Global growth: The subsequent decrease in export volumes and tariff retaliation for impacted economies would also create a negative growth impact outside the U.S., albeit the range of outcomes is broad. Countries most dependent on the U.S. for trade are likely to see the most significant impact: punishing Mexico and Canada, while being milder for China and the EU.

Impact on investors

In the near term, risk-on sentiment may need to contend with an economic outlook of slowing growth, elevated inflation, and ongoing policy uncertainty. So far, companies have navigated the tariff noise without much visible strain, but pressures are likely to grow.

Yet, aggregate corporate sector balance sheets are well-positioned to absorb the headwinds. Overall cash holdings as a percentage of liabilities are elevated, particularly in comparison to historical levels, indicating ample buffers in the event of a revenue or cash flow squeeze. Moreover, profit margins remain high, and overall leverage remains manageable. While there may be some weakness ahead, this is a headwind that the U.S. economy can navigate.

Important Information:

Past performance does not guarantee future results. Investing involves risk, including possible loss of principal. Index performance information reflects no deduction for fees, expenses, or taxes. Indices are unmanaged and individuals cannot invest directly in an index.

Equity investments involve greater risk, including higher volatility, than fixed-income investments. Fixed-income investments are subject to interest rate risk; as interest rates rise their value will decline. International and global investing involves greater risks such as currency fluctuations, political/social instability and differing accounting standards. Real estate investment options are subject to risks associated with credit, liquidity, interest rate fluctuation, adverse general and local economic conditions, and decreases in real estate values and occupancy rates. Commodity futures contracts generally are volatile and not appropriate for all investors.

This report contains general information only and does not take account of any investor's investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding any particular asset allocation, investment product, overall investment strategy, or the markets in general. The information presented has been derived from sources believed to be accurate; however, we do not independently verify or guarantee its accuracy or validity.

Any reference to a specific investment or security does not constitute a recommendation or buy, sell, or hold such investment or security, nor an indication that Principal Global Investors or its affiliates has recommended a specific security for any client. The information contained in this report should not be relied upon as a primary basis for an investment decision and an investment decision based on this report may result in a loss.

The subject matter in this communication is provided with the understanding that Principal® is not rendering legal, accounting, or tax advice. You should consult with appropriate counsel or other advisors on all matters pertaining to legal, tax, or accounting obligations and requirements.

©2025 Principal Financial Services, Inc., Principal®, Principal Financial Group®, Principal Asset Management, and Principal and the logomark design are registered trademarks and service marks of Principal Financial Services, Inc., a Principal Financial Group company, in various countries around the world and may be used only with the permission of Principal Financial Services, Inc.

Principal Asset Management(sm) is a trade name of Principal Global Investors, LLC. Principal Asset Management is the global investment management business for Principal Financial Group®.

This information was created and prepared by Clearnomics, Inc. Clearnomics is not affiliated with Principal Financial Group® or any if it's member companies.

4299248